FinTech communities in Hong Kong and Singapore are coming together at the moment to celebrate exciting new developments in the field of FinTech with the Hong Kong FinTech Week and the Singapore FinTech Festival.

What is Fintech?

Financial technology, or FinTech, refers to the evolving intersection of financial services and technology. FinTech in the APAC region is growing. According to an Accenture report, FinTech investment in Asia-Pacific more than quadrupled in 2015 to $4.3 billion and is now the second biggest region for FinTech investment after North America. Everyone is fighting for a finger in the pie – these tech-driven financial services are provided by startups, technology companies, and even incumbent financial institutions.

FinTech’s Capacity for Growth

With growing support for FinTech in the Asian financial hubs of Singapore and Hong Kong, now is an exciting time to be in FinTech. Singapore’s strong commitment to being a FinTech leader and building a ‘Smart Financial Centre’ is evident in its efforts to nurture the FinTech space.

In a speech at the Singapore Forum earlier this year, the Managing Director of the Monetary Authority of Singapore (MAS), Mr Ravi Menon, stated that the MAS was committed to actively engaging FinTech firms to better understand emerging innovations and help them design their solutions for financial services. The idea is to allow financial institutions to experiment with new technologies in a safe environment and promote greater inter-operability within the industry to harness the full potential of technology.

In Hong Kong, there is growing collaboration between financial institutions and FinTech startups, with the former establishing incubators and accelerator programmes such as the DBS Accelerator and SuperCharger to bring themselves closer to the local startup community and discover innovative solutions to meet their needs. A McKinsey article identified six emerging FinTech trends in China that will continue to drive the industry’s growth:

|

Source: McKinsey

Key Challenges in FinTech

At the same time, FinTech is not an easy space to be in, especially given the number of players – referred to as the As, Bs, Cs, and Ds – in the FinTech ecosystem.

|

Source: PwC

Other than the competition, FinTech firms face several key challenges in growing their share of the pie:

Data security

The nature of FinTech means that companies are often dealing with sensitive customer data. Hacks and security breaches have the potential to undermine your customer’s trust in you. It is thus key that you put in place procedures for access, retention and disposal of data, as well as disclosure of breaches.

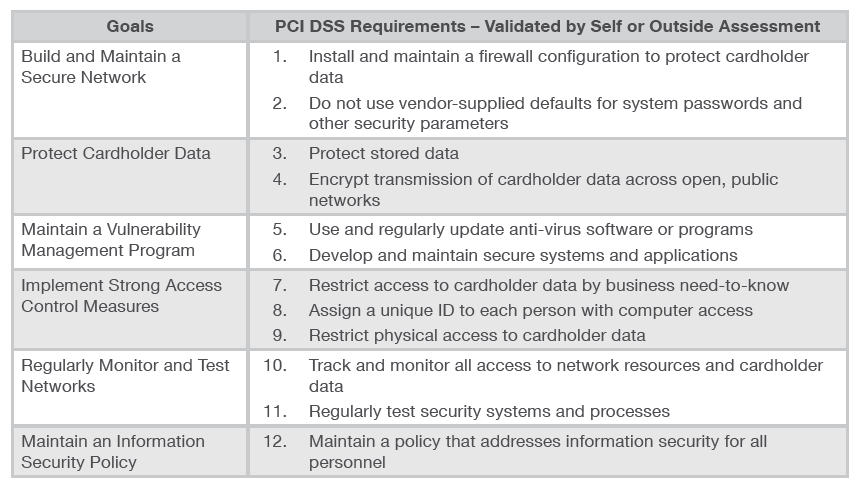

A good reference point is the Payment Card Industry (PCI) Data Security Standard that any business dealing with payment cards must adhere to in terms of storing, processing and transmitting cardholder data:

Source: PCI Security Standards Council

As for how to go about implementing data security standards, the best practices often emphasise 1) implementing clear processes, 2) appointing a designated data protection officer, and 3) constantly updating your security measures and guidelines to keep pace with tech developments. Given that you can never be completely insulated from security breaches, it is essential to develop a plan to adopt and define security mechanisms that will allow you to mitigate specific threats.

|

Source: Bloomberg BNA

Difficulty in scaling

A key imperative of any startup is to scale. Yet, FinTech startups face significant challenges in scaling to capture more of the consumer market, given the nature of the business and the limited resources compared to established incumbents. While many startups are in a hurry to scale fast, this is less likely in FinTech given that consumers are generally reluctant to talk about money. In addition, established financial institutions which are dabbling in the FinTech space have the clients and resources to scale.

In order not to trail behind their larger and more well-funded competitors, be proactive about seeking out experienced advisors with the right expertise. Here are some top tips from Markus Gnirck, co-founder of the leading Startupbootcamp FinTech accelerator in Singapore.

|

Source: Techsauce

Navigating risk & regulatory stakeholders

According to the PwC Global FinTech Survey 2016, regulatory uncertainty is one of the top three challenges for traditional financial institutions and FinTech companies when working together. As there is low regulatory tolerance for lapses on issues such as anti-money-laundering, compliance, and know-your-customer, building capabilities in these areas will allow FinTech players to best position themselves to succeed.

Some industry players regard the fact that regulation has yet to catch up with new innovations as an advantage. At the same time, FinTech startups are vulnerable to legislative updates that might potentially undermine their entire business model. However, the encouraging regulatory environment should be a cause for celebration. The move in Singapore to set up a regulatory sandbox to allow startups to experiment with FinTech solutions within a well-defined space and duration will give innovation the space to flourish – and other countries such as Thailand, Australia and Malaysia are following suit.

It is thus incumbent on FinTech players to leverage on this facilitative regulatory environment. Beyond complying with regulatory requirements, it is crucial for FinTech startups to facilitate regulatory developments by proactively engaging regulators and educating them on your business model. Ensuring that you move along with regulation is part staying ahead of the curve in the FinTech world.

Made for FinTech: Zegal and MKA Law Office

We know it is a challenge to navigate an evolving regulatory environment such as FinTech.

At Zegal, we have prided ourselves on providing more than 5,000 small and medium-sized businesses, general counsels, law firms and business advisors with a better way to manage legal online. Subscribers to our platform have access to any of our 500 existing business documents and can customise them to their specific needs.

At the same time, we recognize that businesses need the help of an expert. In an evolving regulatory environment such as FinTech, startups need good, solid advice on whether they are meeting compliance requirements. As a FinTech company, you want to focus your limited time and resources on developing your product and reaching more customers.

With the newly launched Zegal Managed Accounts, where we partner with established law firms with expertise in a range of industries to provide Zegal-enabled legal services for your organization. A Zegal Managed Account allows you to enjoy the perks of technology, together with an expert who manages your Zegal account for you.

For FinTech companies, our Certified Advisor, MKA Law Office, provides expertise in meeting regulatory requirements and can help you take your business to the next level.

What goes into a Zegal-enabled plan?

- Business compliance: Have your business model or operation documents reviewed on regulatory compliance

- Zegal subscription: Create unlimited legal and business documents on Zegal for the running of your day-to-day business

- Review documents: Have your documents reviewed by experienced lawyers and amended to fit your specific business purpose.

About Author