About Author

Need any help? Contact us:

An Employee Stock Option Plan (ESOP) is a benefit plan that provides company employees with an ownership interest in the form of stocks or shares.

ESOPs provide various tax benefits for the sponsoring company, the shareholders, and the participants.

Employers often use ESOPs as a strategy for corporate finance, aligning the employee’s interests with those of the shareholders and the company.

In other words, an ESOP is a share option plan used by companies to incentivise, sustain, and reward competent employees. Through this share plan, eligible employees can purchase a certain number of shares in the company at an exercise price. Therefore, employees benefit when the share prices for the respective company increase.

Having a share option is not the same as having a share in a company. A share option provides you with the right to acquire shares in a company upon fulfilment of certain conditions.

How does an Employee Share Option Plan operate?

Businesses of all sizes utilise Employee Share Option Plans (ESOPs). In privately owned businesses, ESOPs often play a key role in succession planning. Typically, companies establish ESOPs as trust funds, with the company funding these trusts by issuing new shares.

Additionally, companies might allocate cash reserves to acquire existing shares or may opt to secure financing to buy shares for the scheme.

Contrary to some misconceptions, ESOPs operate on a principle of fairness and do not show preferential treatment to any employees. To ensure the equitable management of these plans, companies must appoint a trustee fiduciary tasked with overseeing the scheme’s operation.

As a result, senior employees do not receive unjust advantages, and all participants in the ESOP have the right to vote.

What are the Tax benefits associated with ESOP?

In the UK, the ESOP schemes that acquire approval from the HM Revenue and Customs (HMRC ) provide tax benefits to both the employer and the employee.

As ESOP participants do not need to pay income taxes, the scheme provides a great incentive for them. The national insurance contribution associated with purchasing shares is much lower than the usual market price.

What does an ESOP comprise?

When establishing an Employee Share Option Plan (ESOP) for your company, it is essential to integrate the following components:

Exercise Price

Within the ESOP framework, employees are offered a predetermined number of options to buy company stock at a set price, referred to as the exercise or strike price. This price is fixed and cannot be lower than the stock’s current market value.

Only upon opting to purchase shares do option holders gain dividend rights and voting privileges. Ideally, the value of shares would be appreciated when employees decide to sell, maximising their financial benefit.

Vesting Period

Ownership of options is not immediate for employees; it is contingent upon completing a vesting period. Only after this period has an option been considered officially vested, granting the employee the right to exercise their option under the ESOP.

During the vesting duration, purchasing shares or enjoying shareholder rights is prohibited. The specific timeframe of the vesting is detailed in the ESOP agreement.

Shareholder Agreement or Deed of Accession

Should an employee whose share options have vested elect to exercise their purchasing right, they transition into a shareholder status.

This change necessitates signing the company’s shareholder’s agreement or a deed of accession, by which the new shareholder agrees to adhere to the terms set out for shareholders within the agreement.

Conditions for Forfeiting Unvested Options

Employees choosing to leave the company risk forfeiting any options that have not yet been vested. Furthermore, the company might mandate the sale of unvested shares to a nominated individual.

Typically, the disposal of options by employees is subject to board approval or specific circumstances, such as company liquidation, as stipulated in the shareholder agreement.

Liquidation Conditions

In scenarios of company liquidation, discretion allows the company to repurchase vested or unvested options from employees.

Employees may exercise their options as part of the liquidation process or opt not to, leading to the options’ lapse or expiration. Those holding shares for over three years are entitled to sell their shares during liquidation.

Additionally, if the majority shareholder opts to sell their shares, they can request employees to sell their shares under similar terms.

Understanding Vesting, Exercise, and Expiration Terms

The implementation of ESOPs is strategically designed to align the interests of employees with those of the shareholders and the broader company goals.

Understanding Vesting, Exercise, and Expiration Terms in ESOPs is an integral aspect of how these plans fit within the broader context of employee compensation and benefits, often detailed in an employment contract.

Employee Share Option Plans (ESOPs) are strategically designed to align the interests of employees with those of shareholders and the overarching goals of the company.

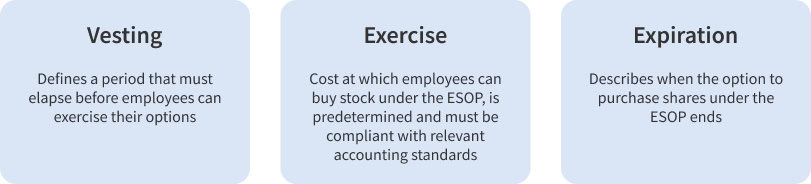

Vesting in ESOPs

A pivotal component of ESOPs is vesting, which defines a period that must elapse before employees can exercise their options. This mechanism encourages employees to remain with the company long-term to benefit from the ESOP fully. Should an employee leave the company before their options have vested, they forfeit any unvested options.

The vesting period’s length, typically ranging from one to three years, is determined by the company’s specific rules for the ESOP, aiming to foster employee loyalty and commitment.

Exercise Price in ESOPs

The exercise price, or the cost at which employees can buy stock under the ESOP, is predetermined and must be compliant with relevant accounting standards. This price is often set to match the stock’s market value at the time of the ESOP grant.

Following the vesting period, employees have the right, but not the obligation, to purchase shares at this fixed price, potentially benefiting from any increase in the company’s stock value.

Expiration of ESOPs

Expiration terms are another crucial aspect, delineating when the option to purchase shares under the ESOP ends. Typically, options expire ten years after vesting or when an employee leaves the company.

The specific terms, including the timeframe for exercising options post-vesting, can vary based on the type of stock options offered (ISOs, NSOs, RSUs) and are important for employees to understand so that they can make informed decisions about their options.

Understanding the intricacies of ESOPs, including vesting, exercise, and expiration terms, is essential for employees to maximise the benefits of these plans. These details are often outlined in an employment contract, which serves as a foundational document outlining the terms of employment and benefits, including ESOPs.

How to Set up an Employee Share Option Scheme

The procedure for setting up an Employee Share Option in your company depends on the laws of the country it operates in, the company’s size, and the scope of the share option plan.

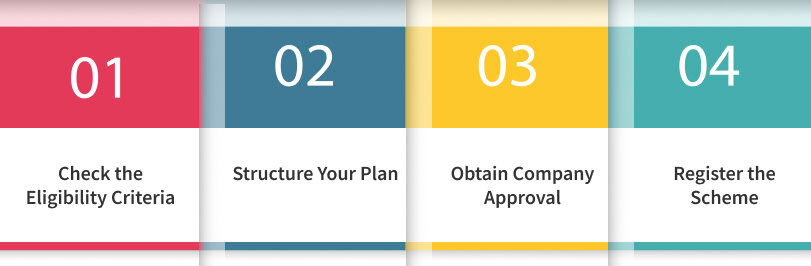

Thanks to technological advancements, establishing an ESOP has become a more straightforward process. Although quick, companies must undertake all necessary steps before involving their employees.

Check the Eligibility Criteria

Before establishing an Employee Share Option Plan, ensure your business is eligible. Legal advice should be sought from practitioners in your country to understand the laws regarding establishing a share option scheme in your company. Eligibility criteria differ widely across countries, depending on the nature and size of your business.

In the UK, your business must have fewer than 250 full-time employees to qualify for an EMI. Additionally, your company’s total assets must be below £30m, and it should not be controlled by or under another company.

Employees must also meet specific criteria to be eligible for this scheme. The company should conduct thorough research before establishing a share option scheme.

Structure Your Plan

When structuring the option plan, companies should consider which employees they intend to include in the plan, the size of the shares, and the Vesting period of the option. As offering options to employees increases the likelihood of new shareholders, companies should assess the impact of share dilution on existing shareholders.

Obtain Company Approval

Corporate authorisation of the plan is required. Once the share option plan’s structure is finalised, the company must approve it. Approval can be obtained in various ways, depending on the company’s structure. You may need the approval of shareholders or the company’s board of directors.

Register the Scheme

The country where your business operates may have specific procedures for registering employee share option schemes. Obtaining official approval is crucial before involving your employees in the scheme.

In the UK, your company’s schedule must be registered with HMRC. If your company operates a company, you can register your ESOP plan by visiting the government website and submitting an EMI notification. This must be done within 92 days after your grant date. Failing to do so could jeopardise the tax benefits associated with the scheme.

What is the Cost of Establishing an ESOP?

The overall cost of establishing an Employee Share Option Plan (ESOP) is typically outweighed by the benefits it delivers to both employees and employers. By aligning the company’s and its employees’ interests, ESOPs can significantly enhance employee productivity.

Beyond these apparent advantages, business owners are also drawn to setting up ESOPs due to their tax-efficient characteristics. Many schemes allow employee options without incurring income tax, making ESOPs a cost-effective way to motivate employees.

When employees exercise their options to buy shares, they typically face a tax rate of only 10% on their profits, considerably lower than the standard 45% income tax rate.

The cost of initiating employee option schemes has substantially decreased in recent years, benefiting both employers and employees.

Previously, establishing EMI schemes could cost a company between £2,500 and £5,000. However, the current market rate for setting up an ESOP plan is around a flat fee of £1,500. Ultimately, the benefits of employee share-option schemes far exceed their costs, offering significant value to all parties involved.

Communicating and Administering an ESOP

When it comes to your company’s share option plan for employees, understanding the methods of communication and administration is essential.

It’s a mistake to assume all employees will grasp the scheme without guidance. Effective dialogue with your workforce is critical to the success of any share option plan.

The importance of communication

At its core, a Share Option Scheme is a form of equity-based compensation for employees. It carries complexities that may take time to be clear to all involved.

Thus, before implementing a share option plan, a company must ensure its employees comprehend the proceedings, benefits, and potential outcomes. In essence, engaging with your target participants is crucial to the success of your scheme.

Large businesses often allocate a significant portion of their budget to effective communication, recognising its value in successfully implementing the option plan.

Employees must understand that equity compensation, including ESOPs, is intrinsically linked to financial factors such as profitability, business cycles, balance sheets, ratios, and the stock market. An option holder’s grasp of these elements may vary, highlighting the need for familiarisation with the risks of share purchasing.

Long-term benefits and awareness

An ESOP serves as a long-term tool to boost employee productivity and align their interests with those of the shareholders. Participation in options providing company ownership means employees should be informed about the company’s status. Lack of awareness could lead to missed opportunities or ill-advised investments in stocks.

The company must communicate any business devaluation or delayed value appreciation due to economic fluctuations during the vesting period. Effectively conveying the nuances of ESOP and financial trends is vital for option holders to understand that valuations are subject to external factors.

Offering equity implies granting employees the chance to become business partners. It’s essential for them to feel invested in the company, which in turn motivates them.

Effective communication strategies

To enhance communication with option holders, companies can employ various methods such as meetings, handbooks, FAQs, flyers, banners, or emails. These can address critical issues like option lapses, vesting alerts, and the end of the exercise period. Providing up-to-date independent valuations of the options is also crucial.

Meeting shareholder expectations is another key aspect of maintaining open lines of communication. For example, during capital raising rounds, option holders might expect selling their shares would yield profit. The company must address and clarify any doubts regarding these expectations.

Corporate actions, particularly those involving changes in control, often lead to situations where investors exit and realise their gains. At the same time, option holders are expected to continue with their options under new investors. Open and transparent communication and fair treatment are paramount to maintaining the original spirit of the options granted to employees.

Research indicates that a third of options lapse due to unaffordable purchase prices or employment termination, leading to premature expiration. Moreover, a lack of education and awareness about Employee Share Options persists. Companies can prevent their ESOP from lapsing by effectively communicating its value to employees.

Practical suggestions for administering ESOPs

Companies setting up an ESOP or issuing options must pay particular attention to several critical areas. One requirement that is often encountered is the provision of a disclosure document to employees.

A disclosure document remains paramount unless specific exemptions apply, such as those for professional or sophisticated investors, small-scale offerings, or senior management.

Deciding on the distribution of ESOP falls within the company’s purview, yet several vital considerations must inform this decision. Foremost among these is the total size of the option pool. Additionally, the employee’s role and expected tenure at the company should significantly influence the allocation of options.

For companies aiming to take advantage of startup tax incentives, it’s crucial to ensure that the structure of your ESOP aligns with the necessary criteria. Various countries offer tax concessions specifically for ESOPs.

For instance, Australia provides tax benefits for ESOPs, while the UK’s tax legislation offers advantages by reducing taxes on employee-owned shares. Ensuring your ESOP meets these criteria can provide significant financial benefits both for the company and its employees.

Tax Implications of an Employee Share Option Scheme

Tax implications when the ESOP is exercised by the employees

When employees acquire shares in their company, exercising their rights constitutes the first taxable event. The taxable benefit is classified under the heading of income or salary.

This benefit can be calculated by identifying the difference between the Fair Market Value (FMV) on the date of exercise and the exercise price assigned to the employee. In many countries, including India, income tax regulations mandate the calculation of the FMV for both listed and unlisted shares.

- Listed Shares: Shares listed on a recognised stock exchange on the date of exercise. For these, the FMV is the average of the opening and closing prices on that exchange. If multiple recognised exchanges exist, the FMV is the average of the opening and closing prices on the exchange with the highest volume of trades.

- Unlisted Shares: Shares not listed on any recognised exchange. For these, the FMV is determined by a merchant banker on the date of exercise or a date up to 180 days before the exercise.

Employer’s responsibility to withhold tax on ESOP benefits

The benefit an employee gains from exercising their option is taxable under salary. Employers are required to deduct such taxes at the time of share allocation, meaning the tax is deducted from the employee’s salary.

This deduction affects the employee’s salary for the month they exercise their rights. To support eligible startups and compensate for employees’ losses, a concession is provided. This concession allows eligible startups to deduct tax from the benefit within fourteen days of the exercise, contingent on specific periods since the start of the fiscal year, from the share transaction date, or when the taxpayer ceases to be an employee.

Eligibility for startups is defined by the laws of the country where the company is based.

Tax implications after the sale of allocated shares

Shares acquired under an ESOP are considered capital assets, and any profit from their sale is subject to capital gains tax. The gain is calculated by the difference between the sale and purchase prices, with the FMV at the time of exercise being considered the purchase price.

The period between share allocation and sale determines if the capital gain is short-term or long-term. Unlisted shares are considered long-term if held for more than two years; otherwise, they are short-term. For listed shares, the period is one year.

Accounting for Employee Share Option Scheme

There are leveraged and non-leveraged ESOPs, differentiated by their financing methods, each requiring different accounting approaches:

- Leveraged ESOPs borrow funds to purchase shares, often from retiring shareholders. The debt is recorded as a liability, decreasing as it is repaid and increasing shareholder equity.

- Non-leveraged ESOPs do not borrow funds; employers fund them directly with cash or stocks, recorded as compensation on the balance sheet. Contributions to the plan are tax-deductible.

Both ESOPs require financial statements to include footnotes detailing funding policies, contributions, expense charges, and covered participants.

Employee Share Option Scheme Benefits for Employees

Employee Share Option Plans (ESOPs) offer a wide range of benefits for employees, some of which are outlined below:

- Wealth Acquisition Opportunities ESOPs provide employees the chance to substantially increase their wealth. As a form of equity option, ESOPs enhance an employee’s financial portfolio by increasing their equity exposure. While bonuses and compensation are beneficial in the short term, ESOPs are designed to generate long-term wealth. Successful ESOP exercises have seen employees amass significant fortunes, sometimes creating generational wealth as the value of acquired shares appreciates.

- Company Ownership Participating in an ESOP allows employees to own a part of the company they work for, transforming them from mere employees to business partners. This ownership fosters a strong sense of belonging and aligns employee interests with the success of the company. The productivity and diligence of employees directly benefit themselves due to their stake in the company, motivating them to contribute effectively and share in the company’s financial gains.

- Strategic Timing of Investments ESOPs offer the flexibility to time investments wisely. Employees can analyse and decide the right moment to invest after their options vest, potentially purchasing shares at a favourable fixed price before share values increase. This strategic investment planning enables employees to maximise returns, minimise costs, and realise potential short-term gains.

How Employee Share Option Schemes Benefit Businesses and Shareholders

Businesses and shareholders derive numerous advantages from implementing ESOPs:

- Enhanced Employee Productivity ESOPs motivate employees to be proactive and efficient. Ownership stakes in the company mean employees directly benefit from the company’s success through dividends and appreciation of share value. This setup encourages all employees, even those without current share ownership, to work towards increasing the company’s value, thus boosting overall performance and benefiting shareholders.

- Providing Exit Strategies for Retiring Shareholders ESOPs facilitate a secure transfer of ownership, ideal for retiring shareholders wary of selling shares to external parties. This transfer method protects sensitive company information and maintains corporate continuity.

- Tax Advantages Both companies and shareholders enjoy significant tax benefits from ESOPs. Contributions to ESOPs are tax-deductible, and companies benefit from tax exemptions on the shares owned through the ESOP. Additionally, loans for ESOP contributions are not taxable, and employees are not taxed on these contributions, mirroring the tax treatment of retirement accounts.

- Attraction and Retention of Talent The vesting period associated with ESOPs incentivises employees to remain with the company longer, providing a compelling reason for talented individuals to join and stay. This ability to retain top talent is crucial for long-term corporate success.

- No Impact on Corporate Governance ESOPs do not affect corporate governance as non-exercising employees do not possess shareholder voting rights. This arrangement allows the company to grow its shareholder base without altering its governance structure or affecting longstanding relationships with partners and clients.

What are the drawbacks of an employee share option scheme?

Implementing an Employee Stock Ownership Plan (ESOP) can present numerous challenges, such as any employee incentive scheme. Some of the drawbacks and challenges associated with an Option Scheme include:

Limitation in Price per Share

The price per share is not constant and fluctuates based on the performance of the business. If the company is not generating viable profits, its value may depreciate, leading to continuous fluctuations in share values. Ineffective management strategies mean employees do not benefit from stock ownership options.

Similarly, if a company’s financial outcomes are inconsistent, employees cannot make informed decisions about exercising their vested rights before the option’s termination. Poor company performance means the share option fails to incentivise employees to invest, nullifying the benefits of an ESOP if the company is not on a trajectory towards profitability.

Issues with Timing

Like share prices, the benefits of stock options are heavily influenced by timing. Employees aiming to maximise their stock options must carefully plan their exit based on the company’s performance.

Exiting when stock values fall results in a lower payout from their option plan. Given the influence of timing, employees must be cautious before selling their shares. Lack of knowledge about stock price fluctuations over time can turn an ESOP into a disadvantage.

Inconsistent Share Values

As the value of stocks is tied to the company’s performance, employees should not rely solely on ESOPs for their financial planning. Instead, they might find it safer to secure their financial stability through retirement savings plans or tax-free savings accounts, which can provide a safety net or additional income.

For those planning retirement, relying on share option plans is particularly risky due to the unpredictability of share values. In essence, employees should avoid putting all their eggs in one basket.

Ideas to maximise the value of an option scheme

ESOPs can contribute to making a business more productive and employee-friendly. Consequently, the popularity of share option plans is increasing in the UK and the USA, with most governments worldwide facilitating laws that accommodate ESOP structures in businesses, such as tax relief on shares contributed to ESOPs or reductions in taxes for shares acquired through stock option plans.

However, their growing popularity only sometimes guarantees employee and company benefits. Before establishing an employee option plan, companies should identify ways to maximise the benefits they can derive from their option plans.

For a budding startup, the valuation of a stock option plan equates to the entire company’s valuation. Companies must report stock option plans as expenses in their profit and loss statements.

For smaller companies, this can be problematic because listing the entire company’s finances as an expense affects the determination of distributable profits, EPS calculation, Minimum Alternate Tax payment, profit calculation for senior management remuneration, and dividend declaration.

How are ESOPs valued?

ESOPs are valued using various methods, such as company assets, income, fair value methods, etc. Hence, their valuation is directly related to the company’s valuation.

Issuing ESOPs over a vesting period also requires valuation. It is important to note that implementing a stock option plan changes the tax structure within the company.

By including ESOPs, which add tax deductions and deferrals, a company can maximise benefits from its stock option plan by deferring income and accelerating deductions, provided its accounting standards allow it.

Proper planning is crucial before setting up an ESOP

Effective organisation is crucial in deriving maximum benefit from a stock option plan. A company needs to appoint an experienced committee to oversee its option distribution. Selecting a skilled and competent advisory team is crucial, meaning a business should hire financial, legal, administrative, and fiduciary professionals to ensure that their ESOP setup offers maximum long-term benefits.

Communicating the intricacies associated with the ESOP plan is also integral to establishing a successful ESOP. Larger companies allocate significant amounts in their budgets solely for efficient communication. This involves educating employees about the company’s valuation and offering them the opportunity to compare the stocks’ market value with their fixed prices, enabling them to maximise benefits from their stock options.

Additionally, employees participating in the option plan but not yet vested with their rights need to be informed about the qualifications concerning the vesting of their stock options, ensuring that the shares allocated to Employee Share Option Plans are not wasted.

Maximising the benefits of an ESOP

The primary step to maximising the benefits of a stock option plan includes having a proper ESOP pool. As ESOPs are intended to increase employee productivity, the company needs to ensure that they are selecting the required and targeted employees for the stock option plans.

An employee needs to have the necessary savings to purchase stocks in the company. Allocating stock option plans to such employees means that the stock option will not be utilised.

The employee and the company can only mutually benefit if they share similar objectives. The final step in maximising the benefits of the employee option plan is to develop and train a competent generation of employees

Risks Associated with Stock Options

Stock Option Plans for employees are an excellent method of boosting a company’s productivity. However, an ESOP setting is not without risks. If you are an employer or an employee considering participating in an option plan, you should be aware of the following risks associated with ESOP:

1. Complexity of ESOP Rules

Implementing the rules and regulations concerning ESOP can be problematic without proper oversight. The operational rules of ESOP are often complex, and companies frequently need to hire third-party operators and advisors to manage a stock option scheme.

Third-party administration may not always prioritise the company’s best interests. It is, therefore, crucial to include an internal agent in the administrative team. Failure to meet the requirements of ESOPs may lead to legal violations, particularly affecting smaller companies and those without efficient accounting structures.

Businesses lacking the necessary infrastructure for setting an ESOP are at risk of breaching ESOP protocols. Thus, if your company does not have the resources and information needed for an ESOP setting, a stock option plan may not be the best option for you.

2. Susceptibility to Fluctuations

If your company has an unstable and unpredictable revenue pattern, your employees may not benefit from the ESOP, potentially leading to counterproductive outcomes.

ESOPs are more suited to companies that do not experience significant fluctuations in their value, allowing stock option holders to make reliable predictions when exercising their vested rights. Companies with volatile patterns are less suitable for stock option plans and are likelier to lay off employees to cut costs.

Providing an equity option to employees may not align with the best interests of such businesses. Even larger companies with stable revenue are not completely shielded from the risks of value fluctuation, and an ESOP could be ineffective during periods of economic uncertainty, such as inflation.

3. Potential Succession Issues

Shares used to establish an ESOP structure are often contributed by shareholders seeking retirement options. As there is no third-party buyer and the share transaction occurs internally, an ESOP can affect internal liquidity transactions.

Likewise, a majority shareholder retiring could mean they are not active in appointing a successor, which could lead to a succession crisis within the company. An owner wishing to retire will need a qualified successor to manage company operations and handle transaction debts.

With a successor, contributing shares for an ESOP is an appropriate strategy.

4. Financial Risks to the Company

If your company urgently needs financing, it would be wiser to involve a third-party investor. ESOP is a long-term solution for company operations and cannot address the immediate financial needs of the company.

The vesting period and the employees’ decisions to purchase shares span a long time and are unpredictable. A company cannot rely solely on its employees for its financial requirements.

While ESOPs provide employees with a share option plan at a fixed price, allowing them to benefit when the company’s stock prices increase, this is a poor strategy for companies seeking to expand financially. An ESOP is unsuitable for companies needing additional capital for sustainability.

5. Incompatibility with Shareholder Interests

Shareholders aiming to maximise cash returns generally seek third-party buyers, such as private companies. In this scenario, share transactions through an ESOP may not align with the best interests of the shareholders.

Shareholders might find buyers willing to pay a premium fair market value. Although ESOP could help increase the company’s productivity by aligning the interests of the employees with those of the shareholders, a company may find more financially advantageous transaction options.

Corporate Governance Considerations with Stock Option Scheme

Companies establish ESOP committees to administer employee option schemes. These committees, also known as administrative committees or ESOP planning committees, are not statutorily defined and are created to structure the stock option plan, as documented in the plan document.

The ESOP committee is tasked with estimating the appropriate scale of the stock option plan to be introduced in the company. They design the plan and provide recommendations to the company’s board of directors. Sometimes, the committee may overlook fiduciary issues such as reducing participant benefits. Other fiduciary decisions by this committee include directing the plans’ trustee in decision-making.

The committee may also hold an advisory role within the company, responsible for communicating the scheme details to participants, allocating participants, and determining the option pool. The committee comprises individuals with expertise in legal and fiduciary matters concerning the ESOP and may or may not include an internal agent.

The company can choose to limit the committee’s role. Sometimes, the company’s board of directors acts as the ESOP committee. Since the board of directors is elected by the shareholders at the annual general meetings, involving the board in the ESOP means that shareholders’ concerns are better addressed.

Regardless of how the ESOP committee is formed, its primary role is to determine matters such as qualification metrics for employees eligible for the ESOP, the terms of vesting, the share price rate, allocation of shares, the suitability of the stock scheme with company.

The Role of ESOP in Stock Option Pools

A stock option pool is a collection of shares set aside for employees of a private company. It serves to attract and retain talented and skilled individuals who are motivated to contribute to the company’s long-term success. If these employees help the company to go public, they are rewarded with shares in recognition of their contributions.

Typically, an employee who joins at the startup phase receives a larger portion of the option pool compared to one who joins later. As the company undergoes subsequent funding rounds, the initial size of the option pool diminishes due to ownership demands from investors. Angel investors and venture capitalists often seek equity in exchange for their funding, leading to dilution of the founders’ shares.

Stages of Growth in an ESOP Option Pool

Early Stage – Aggressive ESOP Strategy

During the seed and angel funding stages, the company has limited liquidity. At this juncture, attracting top-tier executives and critically skilled employees might be challenging due to financial constraints. This is where Employee Stock Option Plans (ESOPs) become crucial. Companies offer ownership options as compensation, enabling them to recruit high-calibre talent without upfront cash. At this early stage, it is essential to offer ESOPs generously, as the primary goal is to build a strong foundational team.

Growth Stage – Focused Cash Strategy

As the business expands and liquidity improves, the focus shifts. ESOP grants should become more restrictive, and the emphasis on cash compensation should increase to meet the rising expectations of employees. During this growth phase, ESOPs should primarily serve to retain exceptionally valuable employees—those whose skills are rare or who contribute significantly to the company’s success. Offering equity to these key employees not only motivates them to commit long-term but also protects the company by discouraging them from exiting and potentially sharing sensitive information with competitors.

Maturity Stage – Balanced ESOP and Cash Strategy

When a company matures, its strategy should balance ESOP grants with cash compensation. By now, the company likely has the necessary infrastructure for sustainable operations and can afford to attract skilled professionals with competitive salaries. However, performance-based ESOP grants still play a role in incentivising peak performance and aligning the interests of employees with those of shareholders.

Role of ESOP in Equity Financing

Equity financing involves raising capital through the sale of shares to shareholders or third-party purchasers, typically without ceding control of the company. ESOP financing, a subset of equity financing, allows employees to own shares in the business they work for. This method helps a company lower its borrowing costs as principal and interest payments on ESOP loans are tax-deductible. Setting up an ESOP involves borrowing money to purchase company shares, which are then held in a suspense account and can be used as collateral for the loan. As the loan is repaid, shares are gradually allocated to employee accounts on a pro-rata basis.

This ESOP structure can take several forms:

- Direct ESOP Lending: The ESOP provides a promissory note to the lender, backed by an employer guarantee.

- Indirect ESOP Lending: The loan is made directly to the company, which in turn lends it to the ESOP, reassuring lenders hesitant to lend directly to ESOPs.

- Non-Leveraged Option Plans: Instead of establishing a loan, the company may opt for a non-leveraged plan, contributing shares directly to the scheme, thus preserving cash flow benefits.

In each case, ESOP financing offers distinct advantages and structures, enabling companies to harness the benefits of employee ownership while managing financial liabilities effectively.

Best ESOP Practices

If you are considering setting up an ESOP structure in your company, it is vital to be aware of practices that can maximise the benefits of the scheme:

- Consult a Proper Financial Advisor

To establish an ESOP effectively, it’s essential to seek guidance from an expert. An experienced financial advisor can provide comprehensive advice on the legal, fiduciary, fiscal, and administrative aspects of setting up an ESOP. Before engaging, ensure discussions about the advisor’s experience, legal fees, and their track record in establishing growth-oriented ESOPs take place. - Establish the Workings of Your ESOP

To develop an optimal plan, the company must assess its needs and organisational structure. Decisions need to be made regarding the type of plan, the amount of stock to purchase, the employee coverage of the plan, and the vesting timeline. It’s crucial to devise a clear and comprehensible ESOP plan, ensuring both the company and its employees derive maximum benefits. - Accommodate Changes in Ownership

Creating an ESOP will invariably lead to shifts in company ownership. It’s important for every shareholder to understand how the ESOP will alter the ownership structure and its implications. Remember, vesting is a protracted process, and ownership status does not change overnight. Allocating options over a three to four-year vesting period, reserving ten to fifteen per cent of the overall ownership for an ESOP pool is advisable. - Obtain a 409A Valuation

A 409A valuation, performed by an independent third party, assesses the fair market value of the equity shares of a private corporation. This valuation is crucial as it sets the price at which employees can purchase shares and ensures that the ESOP is legally sound and equitable, truly reflecting the company’s worth. If working with a professional advisor, they will likely recommend a methodology and may conduct the appraisal themselves. - Acquire Approval from the Board of Directors

Legal recognition of the ESOP requires the approval of the board of directors. Furthermore, anyone with a confirmed financial interest in the company, such as shareholders, should be consulted. This is crucial even if the board has not been formally elected yet. The board’s insight and experience can also ensure that the ESOP is tailored to best suit the company’s needs. - Prepare the Required Documents for Finalization of the ESOP

The company must prepare and compile the necessary documents before finalizing its ESOP. This includes agreements with all option holders, ESOP plan agreements, and option grant agreements. Adjustments may be required in the company’s articles within your business plan to incorporate your ESOP.

Case Study: ESOP of WestLand Resources

In 2021, WestLand Resources, a Tucson-based company with a diverse team from scientists to business experts, achieved complete employee ownership. The company utilized advice from the Menke group to structure their ESOP. The Employee Stock Option transaction was financed through a lateral transfer, a seldom-used method that allows employees to fund their stock purchase using funds from their 401(k) accounts. This mechanism was beneficial for initial funding and securing the future for the company’s employees.

Conclusion

To maximise the benefits from your stock option plan, it is imperative to engage a competent financial advisor and establish clear rules and responsibilities for employees eligible for stock options. Since an ESOP will increase the number of company shareholders and dilute the shares of existing shareholders, the company must be prepared to accommodate new shareholders. It is advisable to obtain a 409A valuation of the company shares before securing the board’s approval. Employing these best practices and learning from relevant case studies will foster maximum growth through your ESOP.