Limited Partnership Funds (LPF) are a new type of fund structure to encourage funds to domicile in Hong Kong by offering a simpler and straightforward regulatory framework. Flexibility in capital contributions, distribution of profits, and contracting freedom facilitates fund management and encourages investment, whilst retaining tax exemption subject to the conditions of the unified funds exemption (UFE)). The new LPF regime places Hong Kong as a premier jurisdiction in which to domicile a PE fund.

Background

The introduction of the Limited Partnership Fund Ordinance (LPFO) replaces the old regime of the Limited Partnership Ordinance (LPO) and it came into effect on 31 Aug 2020. Prior to the enactment of LPFO, there was not much flexibility for the set up of private funds. The private fund managers of Hong Kong had to set up funds constituted in the form of limited partnerships in offshore jurisdictions such as the Cayman Islands and Delaware. The enactment of LPFO is very welcoming and with its introduction, Hong Kong aims to bolster its position in asset management and seeks to cement a place for private equity investment by attracting more fund sponsors.

Initially, the LPFO did not allow offshore funds to re-domicile in Hong Kong. However, funds registered in the form of a limited partnership under LPO were allowed to migrate to the LPFO after meeting the eligibility requirements. Now, LPFO allows even a non-Hong Kong fund set up in the form of a limited partnership to be registered as an LPF under the LPFO after meeting certain eligibility requirements. This whole process validates the pre-existing rights and liabilities of the fund and prevents the creation of a new separate legal entity.

LPFO has simplified the legal structure by removing the onshore/offshore structure and offshore regulatory compliance. There is no need to be regulated by the laws of double jurisdictions as everything is now placed in a single jurisdiction and it has to comply with the laws of only one jurisdiction. The partners of a LPF are not required to engage lawyers of a different place to register a fund as LPF which definitely is both cost-efficient and hassle-free at the same time. This whole process has increased Hong Kong’s competitiveness by this new fund regime by providing an exemption from profits tax, no capital or stamp duty on proceeds, and hence, a simpler regulatory framework.

Having mentioned the key features of this regime, it is worth considering now what is the LPF, the registration process of a fund as an LPF is, advantages of LPF, re-domiciliation of non-Hong Kong funds, migration of funds registered under LPO, and the de-registration process of LPF in the following sections.

What is a Limited Partnership Fund (LPF)?

The fund under the limited partnership fund is constituted in the form of a limited partnership. It can facilitate the establishment of funds onshore in Hong Kong. It is used for the purpose of managing investments for the benefit of investors. Under the LPFO, a “fund” is defined as an arrangement in which:

- the property is managed for business purposes by persons (“operating persons”) on behalf of other persons who do not have day-to-day control over such management (“participating persons”);

- contributions, profits, and income are pooled; and

- returns are distributed to one or more operating persons and participating persons.

REGISTRATION OF FUNDS UNDER LPF REGIME

Requirements for a fund to qualify for registration under the LPF regime

For a fund to be qualified/eligible for registration under the LPF regime. Section 7 of LPFO sets out certain eligibility requirements for this:

- The fund must be governed by a written Limited Partnership Agreement mutually agreed upon by the partners and the agreement is not in contradiction with LPFO or any other applicable law.

- LPF must have a registered office in Hong Kong.

- The fund is not set up for any unlawful purpose.

- LPF must have one general partner (GP) and at least one limited partner (LP).

a) General Partner

The General Partner can be a natural person, a Hong Kong private company, a limited partnership, or a registered limited partnership fund. The following are liabilities and responsibilities of a General Partner:

i) Liabilities of a General Partner:

GP will have the unlimited liability of debts and obligations of funds.

ii) Management responsibilities of a General Partner:

The General Partner is responsible for overall management and control of the funds. The GP can also simultaneously serve as an investment manager and assume the responsibility for carrying out the day-to-day management of the fund. Otherwise, the GP must appoint a separate Hong Kong resident or a Hong Kong company or a registered non-Hong Kong company to act as the investment manager.

The GP must appoint an Anti-money Laundering Responsible Person (AMLRP) to carry out anti-money laundering procedures. The AMLRP can be a legal or an accounting professional, an SFC licensed corporation, or Banking Ordinance authorized institution.

The GP must appoint an independent auditor to conduct annual audits and make proper custody arrangements.

b) Limited Partner

A limited partner in an LPF is mainly an investor who is a natural person, or corporation, or an unincorporated body, or any other entity (acting as a trustee, on its own behalf, or in any other representative capacity. The following are the rights and liabilities of a General Partner:

i) Rights of a Limited Partner:

Limited Partners have no day-to-day management rights or control over the assets of the fund. However, they have the right to participate in the income and profits arising from the fund.

ii) Liabilities of a Limited Partner:

The liability of LPs for the debts and obligations of the fund is limited to the extent of their agreed contributions. However, if an LP is involved in any activity which amounts to the management of funds (not being one of the safe harbor activities that are specified in Schedule 2 of the LPFO) then both LP and the GP may be jointly and severally liable for debts and obligations incurred.

5. The name of the fund must comply with the naming requirements of LPF under LPFO and its name registration will not contravene any restrictions imposed on LPF’s name under LPFO.

6. Partners of funds may consist of other groups of companies.

Registration Application of a fund under LPF regime

Its registration application must be submitted in the prescribed Form “LPF1” along with fees HK$3,034 to the Hong Kong Registrar of Companies by a Hong Kong-registered law firm or through a Hong Kong admitted Solicitor on behalf of the proposed GP in the fund.

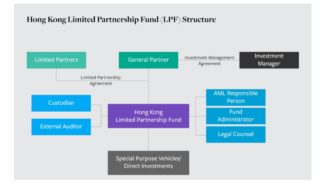

Structure of LPF

Source: https://iqeq.com/insights/hong-kong-limited-partnership-fund-explained

ADVANTAGES OF LPF

- exempted from profits tax provided they meet certain conditions under the Unified Funds Exemption regime.

- No capital duty and/or stamp duty imposed on proceeds arising from the distribution of profits, as well as on the contribution, transfer, or withdrawal of a partnership interest to/from the LPF.

- No requirement to publicly disclose LP’s identity or background information.

- Partners are allowed to contract freely with respect to the operation of funds and all its matters will be governed by its agreement.

- Simplified the legal structure with the removal of offshore/onshore structure and offshore regulatory compliance. Now, everything is placed in a single jurisdiction which results in lower setup fees by removing another layer of service providers.

- Unlike the OFC regime, LPF will not be subjected to approval by the SFC as it is not offered publicly.

- No capital gains tax

- No restriction on the employment of accounting standards at the investment/fund level which means that if a manager is to set up an LPF and he has funds available under management, he may employ his existing standards to ascertain uniformity.

Who will use and benefit from the Hong Kong LPF?

Initially, the primary focus of Hong Kong LPF was on private funds. Its main target was private fund managers who wanted a cost-effective onshore establishment of funds in Hong Kong. They might have earlier constituted offshore limited partnership funds such as in Delaware or Cayman Islands but it didn’t allow re-domiciliation of offshore LPF in Hong Kong. Now, the position has changed as re-domiciliation under the LPF regime is allowed.

Re-domiciliation Mechanism under LPF

Under this regime, a fund that is set up in the form of a limited partnership in an offshore jurisdiction may be registered as an LPF under LPFO.

- The registration process for Re-domiciliation under LPF:

If all the eligibility requirements detailed out in sec 7 of LPFO are met by a non-Hong Kong (offshore) fund then a General Partner in the offshore fund can apply for registration of the fund in Hong Kong. GP can make an application to the Registrar of Companies in the prescribed form LPF10 which is an “Application for Registration of a Non-Hong Kong Fund as a Limited Partnership Fund”. The application fee for registration is HK$3034. The proposed General Partner must submit the application through a Hong Kong law firm or a Hong Kong solicitor who is admitted to practice in Hong Kong. Also, the name of GP must be mentioned in the application as a proposed GP.

- Effect of registering an offshore (non-Hong Kong) fund under LPFO:

The original partnership needs not be dissolved due to registration. The original partnership remains intact. After registration, the original partnership is considered as a registered LPF under LPFO and LPFO applies to the fund. Also, within 60 days of its registration, the Non-Hong Kong fund is required to be deregistered at its place of incorporation.

- Effect of not deregistering an offshore (non-Hong Kong) fund at its place of incorporation/establishment:

The name of the fund may be struck off from the LPF’s register by the Registrar of Companies.

- Is it possible to extend the 60-day time period of deregistering an offshore (non-Hong Kong) fund at its place of incorporation/establishment:

Subject to any condition which the Registrar of Companies thinks is appropriate, the Registrar may extend the 60-day time period on an application by the general partner in LPF.

- Requirement of Business Registration Certificate:

Within one month of the registration date, the GP of LPF must apply for the business registration certificate, if the original partnership doesn’t hold a business registration certificate. If the Non-Hong Kong fund already holds a business registration certificate immediately before the registration as an LPF, it is the responsibility of the GP to notify the Commissioner of Inland Revenue of registration within one month after the registration.

Migration of funds under LPF

Before the coming of LPFO, a fund was registered under the LPO. Now the question arises, is it possible for a fund set up in the form of a limited partnership (specified fund) registered under LPO to be registered as an LPF under LPFO. The following discussion will focus on the migration of funds under LPO to LPFO.

- Registration of fund established under LPO (specified fund) as an LPF:

Where the specified fund registered under LPO satisfies the registration requirements given under s.7 of LPFO, the general partner of the specified fund registered under LPO can make a registration application in the form LPF2 “Application for Registration of a Specified Fund as a Limited Partnership Fund” to the Registrar of Companies along with the fees of HK$3034. The name of GP must be mentioned in the application as a proposed GP in the LPF.

- Effect of registering a specified fund under LPFO

The original partnership needs not to be dissolved due to registration of a specified fund as an LPF. The original partnership remains intact. After registration, the original partnership is considered as a registered LPF under LPFO and LPFO applies to the fund. The registration of partnership under LPO ceases to exist.

- Requirement of Business Registration Certificate:

Within one month of the registration date, the GP of LPF must apply for the business registration certificate. If the specified fund already holds a business registration certificate immediately before the registration as an LPF, it is the responsibility of the GP to notify the Commissioner of Inland Revenue of registration within one month after the registration.

DEREGISTRATION OF LPF

Process of Deregistration

The GP may submit an “Application for Deregistration of Limited Partnership Fund” in Form LPF7 to the Registrar of Companies.

The Registrar will publish a notice in the official Gazette about the proposed deregistration of an LPF. If there is no objection raised to the deregistration within the 3 months of the notice, the Registrar may deregister the LPF by publishing another notice in the Official Gazette. The fund ceases to be registered as an LPF. The Registrar will give notice of the deregistration of the fund as an LPF to the applicant.

Conditions for Deregistration

Each and every partner of the LPF shall agree to the deregistration and the LPF shall not have any outstanding liabilities. Also, the GP is not suing anyone or being sued as an LPF partner with respect to affairs of the LPF in any legal proceedings, and the assets of LPF don’t include any immovable property situated in Hong Kong.

FAQ

-

Can a limited partner contribute money?

The liability of LPs for the debts and obligations of the fund is limited to the extent of their agreed contributions.

-

Can an LPF have its registered office outside Hong Kong?

No, its registered office must be in Hong Kong.

-

How long does it take to issue the Certificate of Registration of Limited Partnership Fund?

The Certificate of Registration of LPF will usually be issued within 4 working days once the application has been submitted.

-

Is a Limited Partnership Fund a legal person?

No, LPF doesn’t have a separate legal personality.

-

Can I get a refund of my fees if my registration application for a fund as an LPF is not successful?

If the application is not successful, the applicant will get a refund of HK$2555 and the remaining amount of HK$479 is non-refundable.

Conclusion

With the introduction of LPFO, Hong Kong has become a prime location for private equity in Asia. The LPF regime not only provides a new and attractive solution to private fund managers for onshore investment but also allows offshore funds to redomicile as an LPF in Hong Kong. The LPF regime is helpful in bringing more funds to Hong Kong and expediting the growth of private funds. It is also amplifying the demand for capital and expertise from different areas like technology and other professional services to create a better base for business opportunities.

Related Articles

Important Documents: Draft now

Follow us on

About Author